Articles/Columns

The Market Voice and Domino Effect Conundrum – How will Japan respond?

In early September, the Swiss National Bank (SNB) announced that it would "no longer tolerate a EUR/CHF exchange rate below the minimum rate of CHF 1.20, and will enforce this minimum rate with the utmost determination and is prepared to buy foreign currency in unlimited quantities". This announcement was quite aggressive, but was probably a necessary step for the SNB to take as a way to deflect the massive surge of deposits into their economy and the massive increase of value of the Swiss franc (Sfr). The deposits had dramatically grown from Sfr 30 billion to more than Sfr 200 billion in just a few weeks prior to the SNB's market intervention. This announcement had the profound effect of dropping the value of the Swiss franc by nearly 8% within just a few hours – such is the power of words when dealing with market speculators. There are many aspects to the Swiss situation, such as protecting its export market and subsequently thousands of jobs. In addition, to alleviate this surge in deposits, the SNB has invested in French and German bonds, rather than bonds from its southern neighbors, notably Spain or Italy. The purchase of these bonds in select European markets communicated to the market speculators a divided Europe – the safe Northern economies versus the doomed Southern economies. Perhaps, the Swiss already know the fate of the Euro, or they are merely speculating themselves. Either way, their actions of buying select European bonds dropped the value of the Euro (due to the Swiss's pessimistic perspective of the Euro zone, i.e. an impending Greek default with rippling effects) and raised the value of the Swiss franc back to its new bottom-line value of Sfr 1.20 (versus the Euro). The Swiss franc no longer seems like a free floating currency, and for the short-term, it will behave similarly to a fixed currency. The long-term perspective is still very much unpredictable, simply because there are too many players in the market. The other perceived safe haven currency is the Japanese Yen. Although the situation is slightly different, the Japanese economy is an export-driven economy and the persistent strength of the Yen at historical levels would seem that the Bank of Japan (BoJ) would also take drastic measures to stem the increasing value of their currency. The BoJ did sell \4.51 trillion in August to soften the Yen's ascent. However, with the major economies in the West entering into a bleak unknown (i.e. U.S. recession, Euro debt crisis), it is quite unlikely that the powerful forces of the Western economies will accommodate a weaker Yen. There are many sources of the current market instability. For example, if China's currency was valued accordingly to actual market value, rather than a 'set' value, then there would be some relief to the Japanese exporters that have been dealing with weaker currencies in most major importing markets, particularly China's (although there have been some advantages associated with investments within their country and abroad). In addition, the re-adjustment from the financial crisis in 2008 is still taking place and with so much complexity, the smart investor can still profit from arbitrage while the regular workers continue to drift due to stagnated wages. In regards to Japan's economy, currently, there is deflation, a huge amount of mostly domestic debt, and a very strong currency. Economically, the simple solution would be to print out some Yen to pay off some of the debt with subsequent effects of bringing back some inflation and weakening the currency. There's no guarantee that Japanese households will spend the extra Yen, rather than lock it away in their second cabinet drawer; so some investment programs should be introduced, such as programs to promote entrepreneurship and innovation, especially in regional markets of Japan, as well as numerous scholarships for studying abroad. However, the ruling elite in Japan have a varying perspective in dealing with its international counterparties and with Japan's recent decline in influential global matters. Executing a currency intervention at a level as severe but different than the Swiss would further isolate Japan from its perceived brethren in the Western markets. Economically speaking, maybe it is time to re-engage with Japan's neighbors and consider how to balance the best interests for not only Europeans and Americans, but also Asians. Exploring strategic tie-ups with Latin America or Africa could also prove to be areas where Japanese investment and manufacturing expertise would be more welcomed than the current trading partners in place. Japan no longer has the economic and political clout to independently bring balance to the global markets, so mutual collaboration is the new norm in moving forward in Asia and in the world.

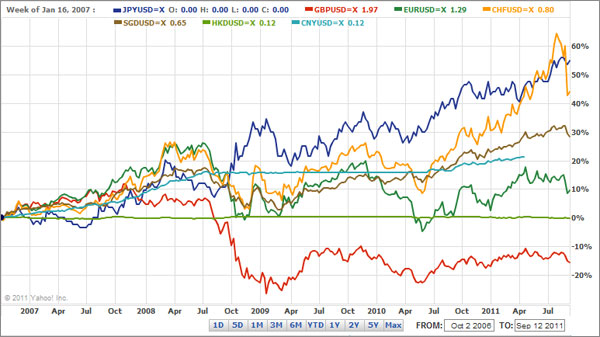

Global Currencies vs. USD

Source: Yahoo! Finance

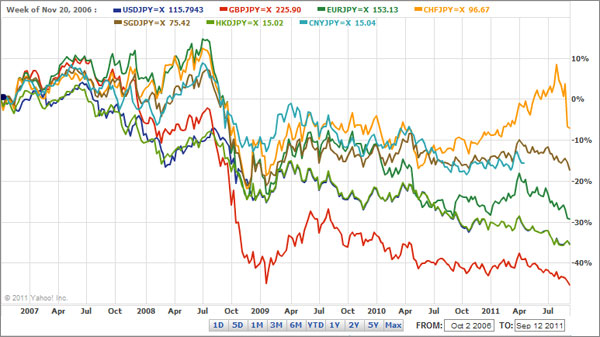

Global Currencies vs. JPY

Source: Yahoo! Finance

(2011/09/27 掲載)